Overview

Drafted by the OECD at the request of the G20 and adopted by around 150 countries since its creation, the international tax reporting standard AEOI (Automatic Exchange Of Information) requires financial intermediaries to declare the tax residence of their clients in the countries that have signed up to the regulation.

CACEIS, its international entities and its clients Asset Management companies, as well as their investors, are therefore affected.

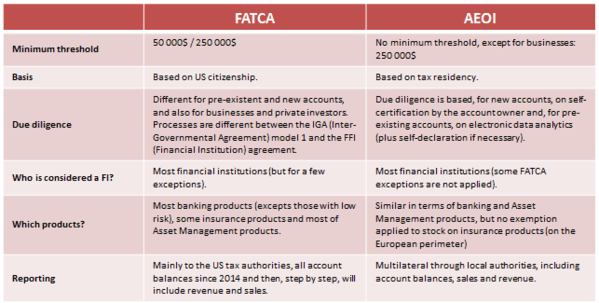

The AEOI goals are identical to those of FATCA:

- fight against tax evasion,

- facilitate the taxation of income received abroad by the authorities of the beneficiary's country of residence for tax purposes.

Since 1 January 2016, financial institutions have to identify all their concerned clients, both natural and legal persons.

The first automatic exchange of information (CRS*, Common Reporting Standard) took place in 2017 in accordance with the OECD standard and concerned data collected in 2016.

The OECD provides information on the AEOI regulation (list of impacted countries, laws and directives by jurisdiction) on its website.

Who is concerned and how?

Private investors and companies holding an account in a country outside their country of tax residence are subject to the AEOI reporting.

Two types of data will be collected by financial institutions:

- Financial data (account balances, interest, dividends, capital gains and any other financial income),

- Reference data (name, main residence address, tax residence address, country, date of birth, etc.).

These reference data will be obtained through a self-certification, made mandatory by the AEOI regulation, should be completed by the account holder (individual or company), signed and sent to the financial institution in charge of reporting to the local tax authority.

In the event of a change in one of the reference data (considered a change in circumstances by AEOI), the account holder must complete a new self-certification to indicate these changes to the said reporting institution.

The standard model of CACEIS is available below. If you are a client of CACEIS or an investor, you must complete it, sign it and send it to your usual sales contact.

Decree of July 3, 2018

On 3rd July 2018, France issued a decree to specify the implementation of additional provisions to the AEOI regulation. This decree specifies that any person, legal or natural, whether a French tax resident or not, who has not replied to requests sent by financial institutions in order to obtain a valid AEOI self-certification, must be subject to two reminders, respecting the sending and response deadlines described in the Decree.

If these reminders are not answered, the person concerned will then be the subject of a new reporting to the Direction Générale des Finances Publiques (DGFIP) by each financial institution before 31st March 2020 for the first time, and then each year on the same date.

Finally, the Decree states that the persons so deferred will be sanctioned with a fine of 1,500 €.

This decree came into force on 1st November 2018 and only covers structures domiciled for tax purposes in France.

Summary table FATCA vs AEOI:

Self-certification

Entities

Individuals